Retirement—those golden years that mark the culmination of a life’s work—should be a time of comfort, security, and, most importantly, enjoying life to the fullest. And it’s not just about reaching retirement age; it’s about optimizing your benefits for a brighter future.

Imagine having the confidence to make informed decisions that could significantly boost your financial security during retirement. Picture yourself leveraging smart strategies that maximize your Social Security, ensuring you have more to cherish those well-earned years.

One such strategy revolves around spousal benefits—a hidden treasure trove within the Social Security landscape that enhances your retirement income, especially if you’re part of a couple. According to Hayes Family Law , legal expertise can be your greatest asset in maximizing your Social Security spousal benefits.

In this comprehensive guide, with a special focus on unlocking the power of spousal benefits. And we will uncover more strategies, understand the impact of crucial decisions, and shed light on the often-overlooked nuances that can shape your retirement income.

Whether you’re approaching retirement or planning ahead, this guide is your key to unlocking the full potential of Social Security.

If you are a parent looking on how to harness the power of spousal benefits to financially secure yourself and have a fulfilling retirement, continue reading:

Table of Contents

Understanding the Basics of Social Security Benefits

Before delving into spousal benefits, it’s crucial to grasp the fundamentals of Social Security. This government program is designed to provide a financial safety net for eligible individuals, primarily retirees, disabled individuals, and survivors of deceased workers.

The benefits are funded through payroll taxes collected during one’s working years, and the amount received during retirement is based on an individual’s earnings history and the age at which they choose to start receiving benefits.

Full Retirement Age (FRA) is a key factor, as it determines the age at which individuals can claim their full benefits; claiming earlier results in reduced benefits, while delaying can lead to increased benefits through delayed retirement credits.

Additionally, grasping the spousal and survivor benefits available within the system is vital, as they provide avenues for spouses and dependents to receive benefits based on the earnings records of the primary worker.

Overall, a foundational understanding of these key concepts is essential for making informed decisions about when and how to claim Social Security benefits to best meet one’s retirement goals.

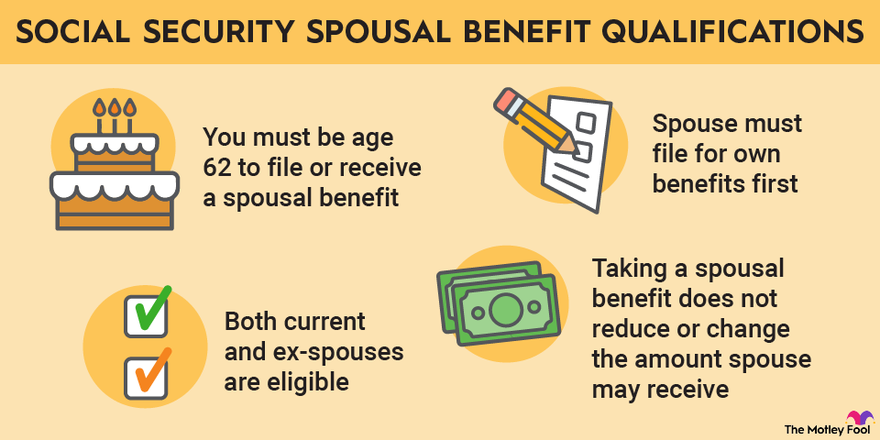

Determining Eligibility for Spousal Benefits

Spousal benefits are available to spouses of primary workers eligible for Social Security benefits.

To qualify you must be: married for at least one year and be at least 62 years old—the earliest age at which one can claim these benefits.

If you have your own Social Security benefits, the Social Security Administration will pay the higher of the two benefits—your own or the spousal benefit.

Understanding these eligibility criteria is essential for maximizing potential benefits for both spouses and optimizing the overall retirement strategy.

Calculating Spousal Benefit Amounts

Calculating spousal benefit amounts under the Social Security system involves determining a percentage of the primary worker’s benefit that the eligible spouse is entitled to receive.

50% Rule: The spousal benefit typically equals up to 50% of the primary worker’s full retirement age benefit amount.

Varying Percentages: This percentage can vary based on when the eligible spouse chooses to start receiving spousal benefits.

FRA: If a spouse opts to receive spousal benefits at their full retirement age, they’re eligible for the full 50% of the primary worker’s benefit. This represents the maximum spousal benefit amount.

Claiming Before FRA: Claiming spousal benefits before reaching full retirement age leads to a reduced percentage. The exact reduction is calculated based on the number of months before reaching FRA when they begin receiving benefits.

Know these calculations to make informed decisions about the optimal time to start claiming spousal benefits in conjunction with one’s own retirement strategy.

Coordinating Social Security Claiming Strategies with Your Spouse

Collaborative planning can yield substantial financial advantages, especially when there’s a significant earnings discrepancy between both spouses.

A strategic approach involves considering factors like:

- Your Respective Ages

- Health Status

- Financial Needs

Alongside the potential benefits of employing techniques like:

- “File and Suspend”

- “Restricted Application”

By synchronizing your claiming decisions, you can optimize benefits by strategically selecting when each spouse begins to receive benefits, leveraging delayed retirement credits, and potentially capitalizing on spousal or survivor benefits.

Professional guidance from financial advisors or Social Security experts can ensure that both spouses navigate the complexities effectively and secure a more financially robust retirement.

Exploring the File and Suspend Strategy

The “file and suspend” strategy within the Social Security framework involves a deliberate approach to maximize benefits for couples.

Higher-Earner’s Move: The higher-earning spouse files for their Social Security benefits at their full retirement age (FRA) but opts to suspend receiving them. This unique step allows their benefits to grow via delayed retirement credits.

Spousal Benefits: Simultaneously, this action opens the door for the lower-earning spouse to claim spousal benefits, typically up to half of the higher-earning spouse’s benefit.

Significant Growth: The result? Substantial increases in the household’s future benefits. The higher-earning spouse’s monthly payments can potentially grow by 8% per year until they reach age 70.

Careful consideration of each spouse’s FRA, financial needs, and long-term goals is essential in determining the most advantageous time to initiate the “file and suspend” strategy. This approach highlights the significance of strategic planning in securing a more favorable financial landscape during retirement.

Considering the Restricted Application Strategy

The restricted application strategy, formerly available to those born before 1954, was a potent method for optimizing Social Security benefits.

Spousal Benefits Focus: This approach allowed individuals to file a “restricted application” for spousal benefits only, enabling them to receive benefits based on their spouse’s earnings while simultaneously allowing their own benefits to accrue delayed retirement credits. This could result in substantial growth of their own benefits over time.

Recent Changes: Recent Social Security rule changes, however, have narrowed the eligibility for this strategy, to those who turned 62 after January 1, 2016.

Understanding these rule changes, evaluating the potential benefits, and working closely with financial advisors or Social Security representatives are crucial steps in navigating the complexities of the restricted application strategy and making informed decisions tailored to one’s unique circumstances.

Understanding the Impact of Divorce on Spousal Benefits

Divorce can have significant implications on spousal benefits within the Social Security system. Individuals who were married for at least ten years and subsequently divorced may be eligible for spousal benefits based on their ex-spouse’s earnings record, even if the ex-spouse has remarried.

However, certain conditions must be met: the individual seeking spousal benefits must be at least 62 years old, unmarried, and the ex-spouse must be eligible for Social Security retirement or disability benefits.

If the divorced individual qualifies for their own Social Security benefits, they would receive the higher of their own benefit or the spousal benefit.

Understanding these intricacies is crucial when planning for retirement post-divorce, as coordinating potential benefits and considering timing become pivotal in making informed decisions about when and how to claim spousal benefits based on an ex-spouse’s earnings history.

Maximizing Survivor Benefits for the Spouse

Maximizing survivor benefits for a spouse within the Social Security framework requires careful consideration of timing and claiming strategies. Surviving spouses can receive benefits based on the deceased spouse’s earnings record, with the choice to claim earlier or later impacting the benefit amount.

Widows or widowers have the option to claim survivor benefits first and delay their own retirement benefits, allowing their own benefits to grow over time.

This strategy can be especially beneficial for a surviving spouse who expects to outlive the deceased spouse by a significant margin.

Evaluating the Effect of Working on Spousal Benefits

Working while receiving spousal benefits can impact your earnings. The Social Security Administration follows an earnings test, temporarily reducing benefits if earnings exceed a threshold.

Earnings Test: The Social Security Administration temporarily reduces benefits if earnings exceed a threshold.

Temporary and Recalculation: these benefits can increase later due to recalculation at full retirement age.

High and Low Earnings: higher-earning spouses’ incomes can affect lower-earning spouses’ benefits through a change in the overall household income.

The interplay between earnings, benefits, and the broader financial context emphasizes the necessity of strategic planning and considering short-term trade-offs for long-term benefits when deciding to work while receiving spousal benefits.

Seeking Professional Advice for Social Security Optimization

Seeking professional advice for Social Security optimization can greatly enhance one’s ability to navigate the complexities of the system and make well-informed decisions aligned with their unique financial circumstances.

Here’s the list of Professionals you can consult:

- Certified financial planners

- Social Security experts

- retirement specialists

They possess the expertise to provide personalized guidance, taking into account factors like age, health, retirement goals, and marital status.

These professionals can help individuals and couples explore various strategies such as maximizing spousal benefits, understanding the impact of timing on claiming, and coordinating benefits effectively.

Their insights can extend to evaluating the potential trade-offs of working while receiving benefits or considering survivor benefits.

Conclusion

Your retirement journey is a testament to your hard work and lifelong efforts. It’s a time to savor the fruits of your labor, and your financial security should never stand as a barrier to your aspirations.

As you conclude this journey through the intricacies of Social Security benefits, remember that knowledge is your most potent tool.

Every decision you make about Social Security, including maximizing spousal benefits, has a direct impact on your financial well-being during retirement. By harnessing the wisdom shared in this guide, you’ve taken a significant step toward securing your future.

Now, seize the moment. Reach out to a financial advisor, schedule a consultation, or embark on a discussion with your spouse or loved ones about the potential of spousal benefits. Your financial future deserves attention and care.

As you stand at the threshold of retirement or continue your path toward it, embrace the power of informed decisions, including the strategic use of spousal benefits.

You’ve learned the strategies, understood the nuances, and grasped the importance of optimizing your Social Security benefits, including this often-overlooked gem. Now, it’s time to put this knowledge into action and your future self will thank you for taking the initiative today.